Pensions Schemes (Conversion of GMP) Act 2022: what it does – and what it doesn’t!

29th April, 2022

-

First introduced in the House of Commons as a Private Members Bill on 16 June 2021, receiving support right across the political divide, and from government, the Pensions Schemes (Conversion of GMPs) Bill is, as of 29 April, now the Pensions Schemes (Conversion of GMPs) Act 2022.

What the Act does

- Clarifies that the GMP conversion process applies to survivors as well as earners.

- Sets out the conditions that must be met in relation to survivors’ benefits.

- Sets out in regulations detail about who must consent to the conversion.

- Removes the requirement to notify HMRC.

What the Act doesn’t

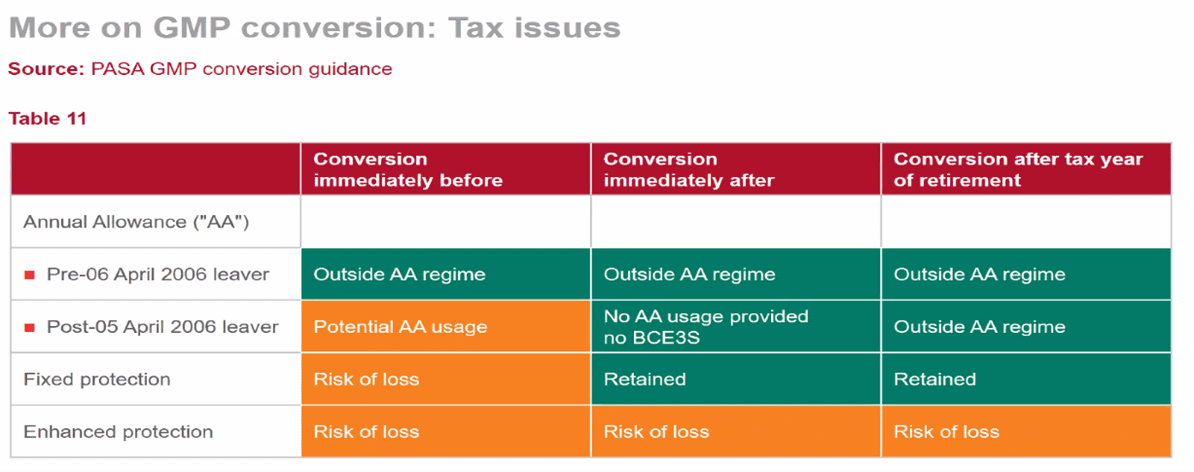

- Cover any of the tax issues related to conversion of GMPs (these issues are illustrated in the table below). It is possible that separate legislation could eventually be passed to address some of the issues but, if it happens at all, it will probably not be until 2023/24.

If the tax issues are addressed then, even if a scheme has already equalised GMPs using a year-on-year method, it would still be possible to subsequently convert GMPs. This could simplify the administration of the scheme and get rid of complexities such as anti-franking’.

Addressing the inequalities ‘arising from GMPs’ does not change the inequalities ‘in GMPs’

Hamill v Lloyds Banking Group Pensions Trustees Ltd[1] concerned a claimant where Equiniti misled him to believe the GMP element of his pension payments would apply from his 60th birthday, before correctly confirming it would not be payable until his 65th birthday. Under the Pensions Schemes Act 1993, GMP age is 65 for males and 60 for females.

However, the claimant refused to accept the corrected stance, despite the offer of a small lump sum for the distress and inconvenience), taking his complaint to the Pensions Ombudsman office, which determined that GMP was payable at 65 (not 60 as argued by the claimant).

Four and a half years later, the claimant sought permission to appeal the determination, which the Court refused, holding that the determination of the Ombudsman was final and binding on the claimant.

A couple of points from this case are of wider interest. Firstly, confirmation that GMP age remains at 65 for men and 60 for women (the 2018 Lloyds Bank GMPE case deals with inequalities arising from GMPs; it does not change the actual conditions for payment of GMPs, which are set out in legislation). Secondly, it confirms the binding nature of Pensions Ombudsman determinations and that decisions of the Ombudsman can only be appealed in limited circumstances.

[1] Hamill v Lloyds Banking Group Pension Trustees Ltd