‘Target End States’ for Defined Benefit pension schemes: What is your final destination?

13th January, 2021

-

A new paper from the Institute and Faculty of Actuaries1 sets out issues trustees, employers and their advisers can consider when addressing whether their ‘Target End State’ (TES)2 should be low dependency, buyout or transfer to a superfund. The key conclusions, using the headings from the paper, along with actions for trustees, are summarised below.

Trustees and their advisers should be considering these in advance of the new Pension Schemes Bill receiving Royal Assent and TES effectively becoming mandatory for schemes.

The role of trustees, the employer and the actuary

According to the TPR/PPF purple book, DB schemes have assets of £1,701 billion at 31 March 2020, backing liabilities on a buyout basis of £2,369 billion, representing circa 5,300 schemes and covering just under 10 million members.

Until recently, there has been little guidance from TPR in terms of what a scheme’s TES should be or how a scheme should progress to its TES. This will change, however, under the new Pension Schemes Bill, which introduces a requirement for trustees to set a Long Term Objective (LTO)3 and also have a plan for how they will get there.

In this section of the paper, it is noted that the various duties and expectations of trustees does mean that they will generally operate in a relatively risk averse manner. However, taking an extremely low risk or no risk approach can mean that a scheme takes longer to reach its TES.

Consideration is then given to actuarial valuations, observing that pension schemes are maturing slowly but steadily, meaning that many are shifting into cashflow negative mode. The endpoint has been crystallised and is generally much more tangible. So, it is timely that, under the Pension Schemes Bill, trustees will, for the first time, be required to articulate their TES.

It is further contended that, the preparatory data and benefit tasks typically carried out for buyout should be done by all schemes, as a part of the work to achieve the TES; otherwise TES and member benefit security is put at risk.

For sponsoring employers, the paper states that the employer has a key role to play in determining the TES for their scheme, the pace in which that destination is reached, and the actions taken in that journey. So, trustees and employers must understand the relative balance of key powers within their scheme rules.

The paper adds “Employers would be well advised to undertake a legal review of scheme rules long before surplus arises and include rule amendments to protect their interests should a confirmed buyout surplus arise.”.

Related to this is the possibility that desirable activities to de-risk schemes are deferred, or even curtailed, for no reason other than the potential impact on the employer’s financial statements.

It is envisaged that the future role of the actuary, working with other advisers, will be pivotal in helping trustees to understand how to bring together the necessary funding, investment and covenant considerations.

The employer covenant still matters

This section of the paper (chapter 3) emphasises the continuing importance of employer covenant and also its impact on the amount of time a scheme has to realise its TES. It is important in the strategic direction of a scheme and not just in financial support. It is stated that – “To develop a TES strategy, trustees need to consider principally:

- The long-term viability of the employer covenant

- The implications on the scheme of an employer covenant failure

- The downside protections available (e.g. third-party guarantees, collateralised support).”

- Recognising that covenant visibility is likely to be limited to the medium-term in most cases, the paper includes some practical suggestions on what trustees can do to better understand and mitigate key covenant risks.

Low dependency

This approach to discharging the trustees’ duty (known by various names including – runoff, self-sufficiency, low dependence and low reliance) entails the continued payment of benefit outgo from the assets. The scheme is then wound up when the last payment has been made, or at a pragmatic point before then, when the assets have become small with remaining liabilities secured with a buyout.

This part of the paper aims to help trustees clearly define a low-dependency TES by understanding different approaches, investment strategies and other key considerations, including scheme size and scale. The paper argues that, when considering low dependency, there is a need for a more rounded view.

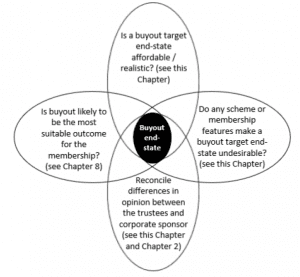

Buy-out

Chapter 5 of the paper starts with the observation that, whilst buy-out is often described as the “gold standard”4, the legal duty of trustees is not, necessarily, to target securing pension entitlements with an insurer. This section then goes on to consider why trustees might or might not choose to target a buy-out and, for those schemes targeting buyout, how issues they need consider differ to those schemes targeting a low-dependency TES. There is a useful summary of activities relating to the journey plan for buy-out, as well as a nice illustration of some key considerations.

Superfunds

This section considers the commercial consolidation vehicle or “superfund”5 as a TES option.

A key difference and challenge with superfunds is they do not offer a common proposition (whereas the buy-out product is “relatively vanilla”). That said, a superfund transfer is a transactional TES just like buyout and so many of the factors relevant to a buyout are also relevant here, albeit in a different way.

Member outcomes

Chapter 7 is concerned with the level of benefit entitlements ultimately received by members, compared with those promised under the scheme rules (‘member outcomes’).

It is contended that funding levels are “at best a simplistic, indirect assessment of Member Outcomes, and we need more sophisticated, granular tools to be able to help trustees and employers navigate between the TES options available to them”.

The introduction of superfunds is cited as a reason for more comprehensive member outcome analysis, but the paper also states “in depth analysis of Member Outcomes is key to support decision making relating to any non-trivial or obviously positive activity, not only where a transfer to a superfund is on the agenda”. It then sets out an approach to measuring member outcomes, looking at the level of benefits members are projected to receive, compared with their full benefit entitlements, and how those outcomes vary by different categories of members, over different timeframes, and under different TES’.

Choosing between the Target End States

The TES’ relevant to most schemes are covered in the paper. All three would normally meet the requirements for discharging benefits, but they do so in very different ways.

Chapter 8 sets out a five-step approach to determining the appropriate TES for a scheme as follows:

- Use a long-term Integrated Risk Management (IRM) framework to identify which of the trio of TES are in play and the Journey Plans that would get the scheme to those TES.

- Understand any requirements, constraints or other factors that may impact the choice of TES.

- Model for different Member Outcomes under the TES in play in the event of the employer default.

- Eliminate any TES or Journey Plans that are not desirable.

- Determine the preferred TES from those remaining after which the Journey Plan can be refined and a plan of action developed.

In all events, trustees should be aware that the Pension Schemes Bill will require all schemes to document their “funding and investment strategy” (amongst other things) in a “statement of strategy”.

So, TES will become a ‘must have’ rather than just ‘nice to have’.

Once a TES is attained, this is not necessarily the end. Trustees should review their TES on a periodic basis to check it remains suitable and, as they get progressively closer to it, to decide whether that is where they will stop or whether it is the first milestone in a longer journey. Also, the TES is not just about the financial position of the scheme. According to the paper “There are a multitude of areas that impact how a scheme is run and hence the effectiveness of its journey to the TES and Member Outcomes. Once the TES is known a broader management plan should be developed”.

Stressed schemes

This part of the paper considers schemes where the focus becomes one of maximising outcomes for members in light of the circumstances in which the scheme finds itself, even if those outcomes are not full benefit entitlements. Trustees of stressed schemes should refer to Chapter 9 of the paper.

- The clear actions arising from this paper for trustees and their advisers encompass:

- Data audit

- Balance of power audit

- Review of rules on surplus

- Advice and strategies around employer covenant

- Defining and understanding the relevance of ‘low dependency’

- Defining a buyout TES

- Defining a superfund TES

- Measuring member outcomes

- Choosing between different Target End States

- Reviewing the TES

- Development of management plan